Look outside your window. If you see a house to your left, right and across the street then you have Alfred Levitt and his father, William, to thank. Credited as the fathers of modern American suburbia, they were entrepreneurs and builders that would forever alter the way we build and purchase property.

A typical Levitt house of the late 1950s

Before World War II, suburbs did not exist the way we see them today. Plots of land were bought, built on and sold but whole communities were not give a single title and there was no unification. Being men of vision and development experience, William and Alfred Levitt made their pre-World War II riches by building upscale housing on and around Long Island, New York. Levitt & Sons became known as the premier developer in that area, buying up farm land and selling homes to the upper middle and wealthier classes. During and after his service as a Navy lieutenant, William Levitt observed a crisis in housing. Young soldiers were returning with hefty government loans looking for new homes in which to raise their families. They needed something affordable and they needed it quick. William Levitt's solution was to mass produce inexpensive homes that would be in close proximity to each other.

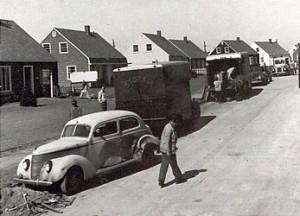

In 1941 the Levitts were granted a government contract to build 2,350 homes for defense workers in Norfolk, VA. With the help of his father, William and his team went on to build an even larger community on Long Island in 1947 which included 17,000 homes all on only 7.3 square miles of land. They called this Levittown and maintained rigorous parameters, each

property had exactly 2 trees in its front yard spaced a specific amount apart. They were either Cape Cod or Ranch in style, 750 square feet and consisted of 2 bedrooms, a living room, a kitchen and an unfinished second floor with no garage. All homes came with a washing machine and television included.

Levittown, New York, October 1947

To keep production costs low, strict standards had to be maintained. Specialized teams were created where each individual had one very specific task that they would complete on each house in a predetermined order and at a specific pace. First cement was mixed and lumber was cut on-site. Then the carpenters, tilers, painters and roofers arrived in sequence. This allowed the Levitts to build up to 180 houses a week while maintaining relatively excellent quality. To save money on materials, they bought forests and constructed their own saw mills. They purchases appliances directly from manufacturers and even made their own nails. At the beginning, these houses sold for between $6,995 and $8,000, easily affordable with a mere $58 down payment.

The Levitts continued to build suburban communities in Pennsylvania, Puerto Rico and New Jersey and ultimately built more than 180,000 houses. At one point they boasted a production record of one suburban house every 16 minutes. Standing among economic greats like Henry Ford and his automobile assembly line, the Levitts did not just sell houses, they manufactured and marketed the American Dream of stability and security and sold it to Americans at a price they could easily afford.

Pod House by Hans Haus with 4 rooms that rotate into view from a cylinder in the center

In 1968, Levitt & Sons was sold to ITT International Telephone and Telegraph for $90 million. Still relatively affordable, though surely showing their age, Levitt houses were still selling for around $155,000 in the late 1990s. But the concept of the suburb has remained an important and desirable fixture in housing markets ever since with new developments being created all the time.

With the emergence of eco-friendly "pods" and extra cost and space efficient homes now growing in popularity, it is clear that the legacy of the Levitt family lives on.

Header Social